How much is bike insurance? Cost of bike insurance

.png)

Looking for insurance to cover your new two-wheeler? Let’s find out how much is the cost of bike insurance in India and what all purposes it serves in this post.

Vehicle insurance is a must if you want to ride your bike or car on the Indian roads. So, if you are planning to buy a two-wheeler, you must start looking for bike insurance online for your new vehicle. Let us find out in this post how much you need to pay for your two-wheeler insurance depending on the plan you choose and what purpose it serves you.

Two-Wheeler Insurance

When you buy a two-wheeler insurance, the premium charged by the insurer depends on various factors such as age of buyer, make and model of bike, coverage opted for, location, bike driving and claim history of the buyer etc.

The obligatory and the most cheap bike insurance plan is the third-party liability insurance. This plan covers the insured for the damages and liabilities caused to the third-party person and property. However, it doesn’t cover for damages caused to your own vehicle. Comprehensive policy, on the other hand, is one that allows both third-party and your own damages in the most comprehensive way. So, the vehicle owner should buy the most useful and cost-effective policy after making proper comparisons and assessing the needs.

6 Basic Points Why you Need a Bike Insurance

- Because it is mandatory

- It covers many important aspects like natural disasters such as flood, earthquake, fire etc.

- It covers against damages done by men in the form of riots, terrorism, theft etc.

- Bike insurance secure the policyholder against various damages that might turn up on the road while riding the bike

- You gain greater benefits and security as compared to the premium charged by the insurer

- Premium charges are also decided by the insurer depending on various risk factors.

Two-wheelers & Insurance premium charges

To understand the approximate cost of bike insurance and how they are calculated based on different variables like make and model of vehicle and engine capacity, we are providing a chart below. It contains the top two-wheelers in the market at present and their average insurance cost. However, you must note that other variables like mileage, maintenance, age of bike owner etc. also affect the insurance premium price of a bike.

Below is a table showing different bikes and their insurance premiums:

| Two- wheeler type | Engine Power | Price of bike | Premium (avg.) |

| Honda Activa | 110cc | INR 65,000/ | Between INR 1350 to INR 1750 |

| Bajaj Avenger | 220cc | INR 1,00,000/ | Between INR 1800 to INR 2000 |

| Hero Honda Splendor | 125cc | INR 70,000/ | Between INR 1300 to INR 1800 |

| TVS Apache RTR | 180cc | INR 90,000/ | Between INR 1750 to INR 2300 |

| Yamaha Fazer | 149cc | INR. 1,70,000/ | Between INR 1550 to INR 2200 |

Let us check the various variables that affect a bike insurance premium in detail below.

Factors that Affect cost of bike insurance

- Make and Model of bike – As already discussed, premium of bike insurance depends on the model and make of the bike. For instance, sports vehicle or high end vehicles or bikes are charged with greater premium than the normal ones

- Deductible amount charged – Deductible is another factor that affects the premium. If you keep the deductible as high, you may pay a low premium. However, in this case the repair cost will be more from your pocket. So, it important to consider this aspect before setting the deductible amount

- Coverage opted for – Likewise, if you avail the minimum coverage of a third-party liability policy, the premium will be less costly as compared to availing comprehensive coverage, which cover third-party as well as your own damages

- Safety devices or anti theft devices fitted in the bike – Use of safety gear in your bike like anti-theft devices etc., also allow low cost of bike insurance as it lowers the premium of the policy

- Age of the bike owner/insured – Insurance providers are of the view that the younger the rider, the higher the risk. So, they levy greater insurance amount for young bike owners as compared to the matured people

- Age and condition of vehicle – Age and condition of vehicle is also important in terms of deciding the premium of your bike insurance

- Availability of NCB or No Claim Bonus – If you have managed to gain some NCB discounts on your policy, it can be used to lower the premium of your bike at the time of bike insurance renewal. NCB is offered by insurers if the policyholder doesn’t claim any insurance amount in a particular policy year. It supports lowering your bike insurance renewal cost.

Let us now consider some tips that can be used by policyholders to reduce their two-wheeler insurance policy.

Tips to Reduce Cost of bike insurance

- The smaller the bike the lighter the premium load – If a compact bike with low engine capacity can fulfill your requirements, go for it to avail lower premium. Since fancy bikes with greater engine capacity will definitely have higher premium amount levied on the insured

- Do not consider any bike modification – Avoid modifications in your bike if you do not want to pay extra amount of premium since modified bikes are generally more expensive as they have high cost of repair

- Pay premium in lump sum – If the insurance premium is paid in lump sum amount, the insurer might allow a certain discount on it. Also, buying long term bike insurance policies of 2-3 years or beyond, you may have some discount on the premium

- Do not go for additional riders – If it is not required, avoid getting any additional riders or add-on policies on your bike insurance. This way you can lower the cost of bike insurance renewal to a certain extent.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Other Motor Insurance Products

Latest Post

You're sitting with your CA on July 28, ready to file your IT return. Your CA asks, "Do you have all investment receipts?" You scramble through documents, realizing some proof is missing. This panic is avoidable.

Buying bike insurance online used to seem complicated. But today, purchasing coverage for your two-wheeler is simpler than ever. The challenge now isn't availability—it's choosing the right bike insurance from dozens of options.

Insurance is an important financial safety net that protects individuals and families against unexpected medical expenses, accidents, loss of income, and other financial risks.

.png)

It's June. The monsoons are here. Suddenly, you develop high fever, body aches, and headache. Your doctor suspects dengue. Your first concern after "Will I be okay?" is "How much will this cost?" This is a question millions of Indians face annually, especially during monsoon and post-monsoon seasons when dengue cases spike.

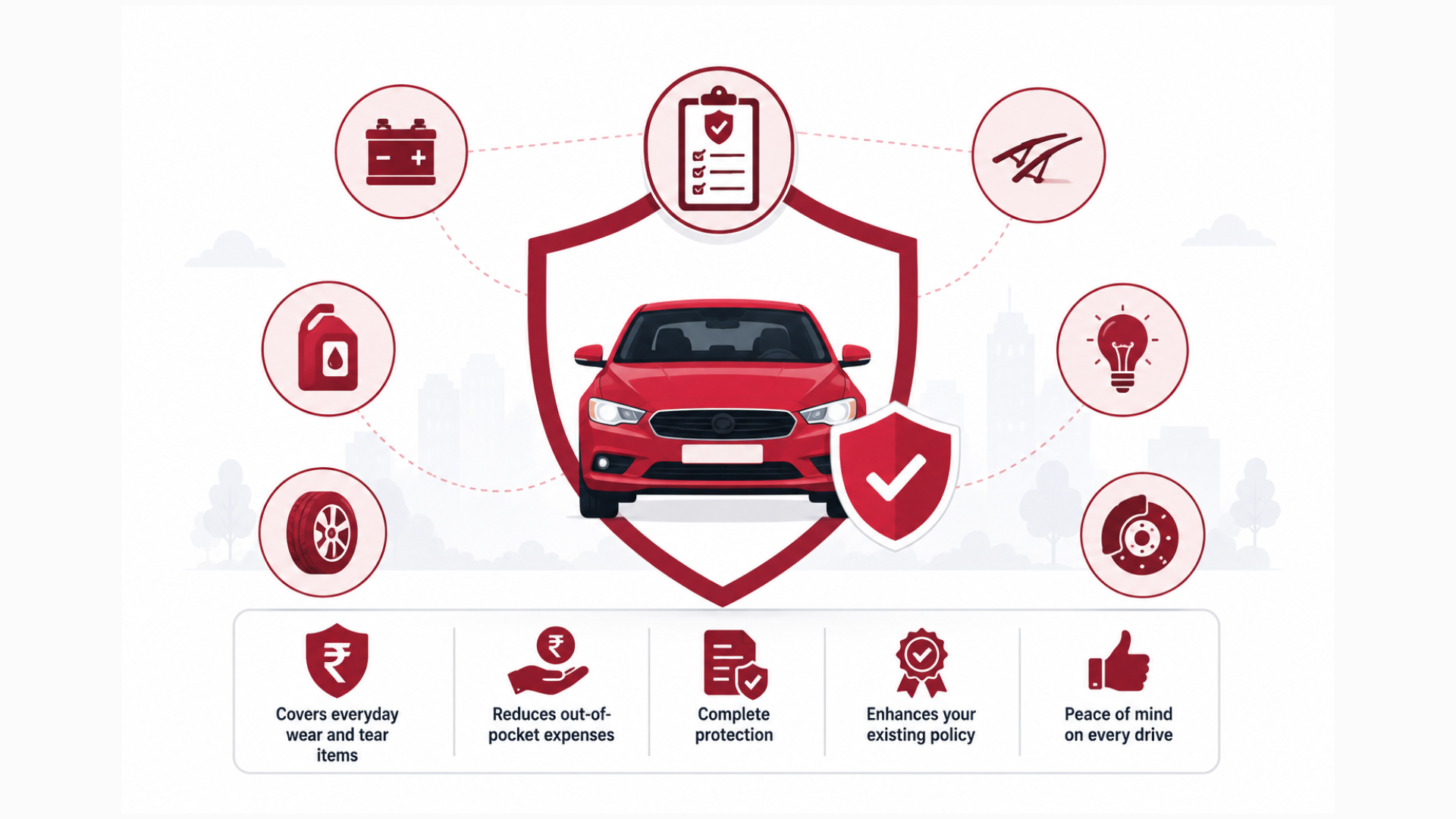

You've just purchased your dream car. You maintain it religiously—regular washing, polishing, timely servicing.

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.