Related Articles

You have finally done it – you have bought a comprehensive car insurance plan to cover your prized vehicle, thinking it’s the golden ticket to complete peace of mind. “I am covered for everything”, you might say, confidently revving up your engine. But what if we told you there is more than meets the eye?

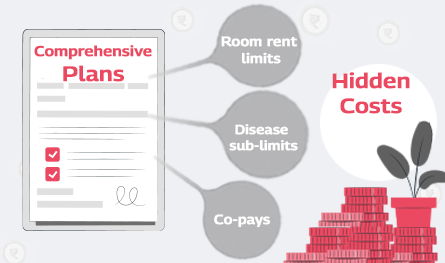

If you have ever filed for an insurance claim, chances are you have noticed that the payout was not quite what you hoped. Car insurance hidden charges can sneak up like a speed bump on a rainy night – annoying, unexpected, and definitely something you would prefer to avoid. This article will go over the top 5 hidden traps that could be nibbling away at your car insurance – and how to steer clear of them.

You may have noticed your premium creeping up, or maybe your claim amount didn’t match what you thought you were entitled to. Just because your car insurance plan is called “comprehensive” does not necessarily mean it is completely transparent. “Comprehensive” does not always mean clear-cut. Underneath all that coverage could be some clever fine print that adds a few unexpected costs to your policy.

Here is a list of the top 5 car insurance hidden charges:

If you want your motor insurance to genuinely go the distance for you, it's time to look beyond the brochure. Here is the list of a few pointers to keep in mind when buying motor insurance:

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Secure your daughter’s education and marriage in 2026 with LIC’s top child plans. This updated guide has detailed tables, real examples, more features like loans and riders, plus smart tips. Read and plan confidently!

ITR filing for 2026 can feel confusing with income mismatches and form issues. This detailed, simple guide helps working professionals and families avoid costly errors, claim full refunds, and build long-term financial security.

Tax season can be stressful, but avoiding these common ITR mistakes helps you claim rightful refunds faster and stay compliant. Learn practical advice tailored for working professionals and families in India.

Empowering women with financial security! Explore top LIC policies in 2026 tailored for savings, life cover, and family protection. Ideal for working professionals, homemakers, and mothers aged 25-55.

In today’s busy world, keeping track of your life insurance is important for financial security. This easy guide shows how to check your ICICI Prudential policy status quickly so you can manage investment plans, term plans, or guaranteed return plans without stress.

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.

Car Insurance

Car Insurance