Everything You Should Know About the Term Insurance Grace Period

Discover everything about the term insurance grace period – from IRDAI-mandated durations to revival processes. Learn how online term insurance provides affordable, high-coverage protection like 1 crore term plans without the complexity of investment or guaranteed return plans.

Why Term Insurance Matters for Your Family’s Future

In today's uncertain world, securing your loved ones' financial future is a top priority, especially for individuals aged 25 to 55 who are building careers, raising families, or planning for retirement. Online term insurance has become one of the most popular and affordable ways to get substantial life cover at low premiums.

A 1 crore term plan, for instance, can provide your family with a significant safety net for just a few hundred rupees per month, depending on your age and health. Unlike investment plans or guaranteed return plans that combine savings with protection (often at higher costs), pure term plans focus purely on life coverage. Child insurance plans or comprehensive life insurance plans can complement this, but term insurance remains the foundation for high protection at low cost.

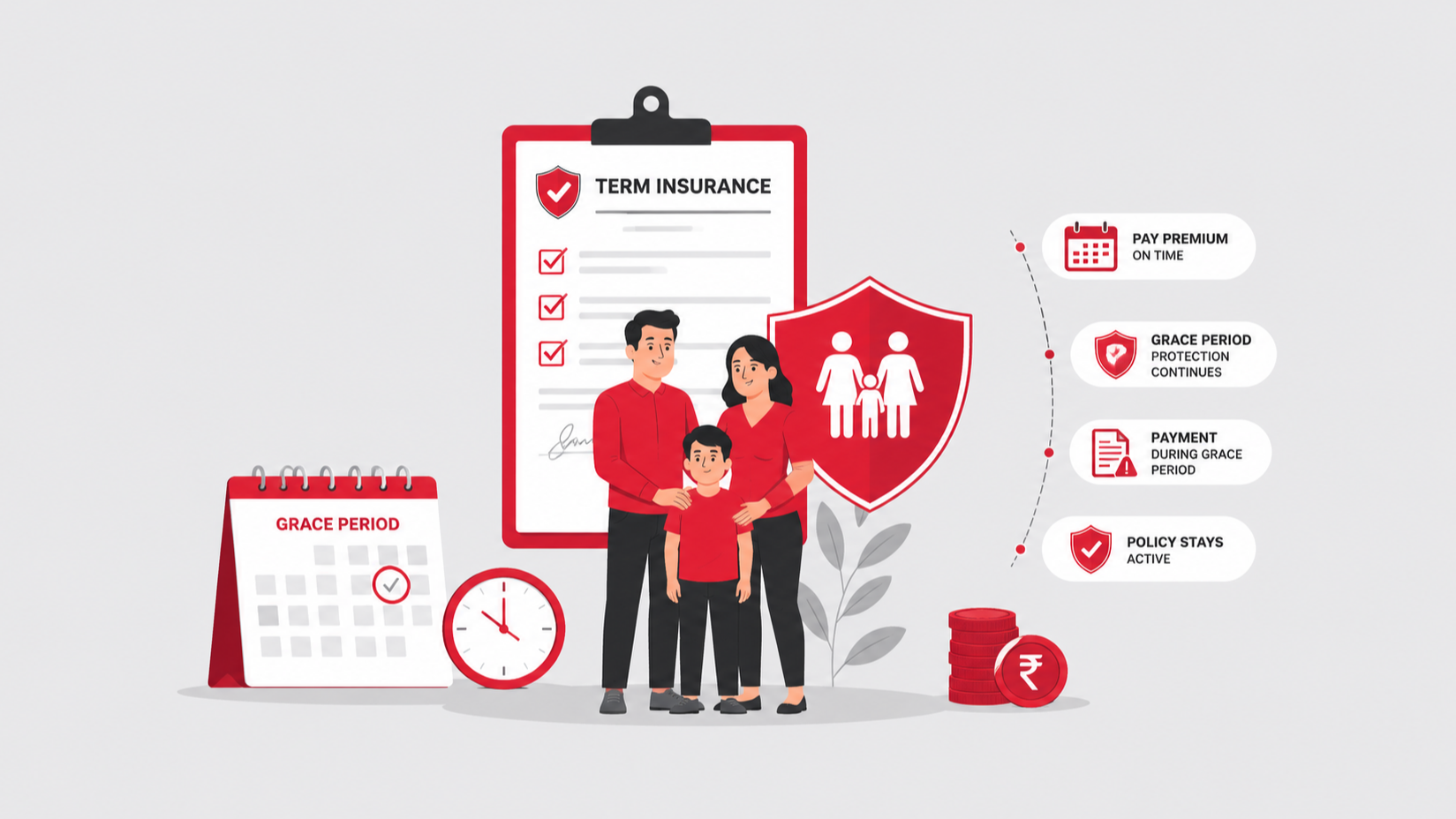

One crucial yet often overlooked feature is the term insurance grace period. This safety net prevents your policy from lapsing immediately if you miss a premium due to temporary cash flow issues. Understanding it can save your coverage and give peace of mind.

What is the Term Insurance Grace Period?

The grace period in a term plan (or any life insurance policy) is the additional time insurers give you after the premium due date to make the payment without the policy lapsing. During this period, your coverage remains fully active. If the insured person passes away during this time, the nominee can still claim the full sum assured (minus any due premium in most cases).

This provision, mandated by the Insurance Regulatory and Development Authority of India (IRDAI), protects policyholders from accidental lapses due to forgetfulness, banking delays, or short-term financial hurdles.

Latest Statistics and Trends (2026 Context)

India’s life insurance sector continues its steady expansion in 2026, driven by rising awareness, digital adoption, and the growing preference for pure protection products like online term insurance. Here’s a snapshot of key figures:

Key Industry Statistics Table (as of FY 2024-25 / Projections for 2026)

| Metric | Value (FY 2024-25) | Projection / Trend for 2026 | Source Notes |

|---|---|---|---|

| Total Life Insurance Premium Income | ₹8.86 lakh crore | 8–11% growth expected | IRDAI Annual Report |

| Market Size (Life + Non-Life) | ~USD 142–156 billion | USD 156.2 billion in 2026 | Mordor Intelligence |

| Life Insurance Share | ~71% of total insurance market | Continued dominance | Industry Reports |

| Insurance Penetration (Overall) | 3.7% | Gradual improvement targeted | IRDAI |

| Life Insurance Penetration | 2.7% | Still low vs global average (~7%) | IRDAI |

| Claim Settlement Ratio (Industry) | 98%+ for top players | High 95–99.5% range for leading insurers | IRDAI & Company Reports |

| Term Insurance Uptake | Rising significantly | Strong growth in online & 1 crore+ covers | Market Trends |

| Private Sector Growth | 12.07% | Outpacing public sector | IRDAI |

Additional Insights (2026 Context):

The Indian life insurance industry recorded a 6.73% premium growth in FY 2024-25, with private players growing at 12.07%. New business premiums and digital channels are fueling momentum. Online term insurance has seen particular traction among the 25–55 age group due to its affordability and convenience.

Many professionals now opt for 1 crore term plans or higher, with premiums starting as low as ₹13–15 per day for young buyers. The average sum assured in term policies continues to rise, reflecting better financial awareness. Digital direct-to-customer (D2C) sales of term insurance grew notably, supported by instant issuance and paperless processes.

High claim settlement ratios (often 98–99.6% for top insurers like Max Life, HDFC Life, ICICI Pru, and Tata AIA) have built strong consumer confidence. This reliability encourages more people to choose pure term plans over complex investment or guaranteed return plans when protection is the primary goal.

Term insurance trends in 2026 include customizable riders (critical illness, accidental death, disability), flexible payout options, and bundled multi-benefit covers. Insurance penetration remains an opportunity area — at just 3.7% overall, there is significant headroom for growth, especially in tier-2 and tier-3 cities through online platforms.

IRDAI Rules on Grace Period (Latest as of 2026)

As per standard IRDAI guidelines (unchanged in core structure through 2026):

-

Monthly premium mode: 15 days grace period.

-

Quarterly, Half-yearly, or Annual modes: 30 days grace period.

These are calendar days, starting the day after the due date. Coverage continues during this window. No late fees are typically charged within the grace period, but the due premium must be paid to keep the policy active.

Note: Always check your specific policy document, as minor variations may exist by insurer, but IRDAI sets the minimum standards.

Table: Grace Period by Premium Payment Mode

| Premium Payment Mode | Grace Period (IRDAI Standard) | Coverage During Period? |

|---|---|---|

| Monthly | 15 days | Yes |

| Quarterly | 30 days | Yes |

| Half-Yearly | 30 days | Yes |

| Annual | 30 days | Yes |

What Happens During and After the Grace Period?

-

During the Grace Period: Policy stays active. Full death benefit is payable if a claim arises (subject to policy terms).

-

If You Pay Within Grace Period: Policy continues seamlessly. No impact on future benefits or bonuses (if any).

-

If You Don’t Pay: The policy lapses. Coverage stops. To reactivate, you may need to go through revival, which could involve medical tests, interest on overdue premiums, and possible underwriting.

Important for Death Claims: If death occurs during the grace period, most insurers pay the claim after deducting the overdue premium. This is a key protection.

Why the Grace Period is Especially Useful for Online Term Insurance Buyers?

When you buy online term insurance, the process is quick and paperless, with instant policy issuance in many cases. However, busy professionals (common in the 25-55 age group) might miss reminders. The grace period acts as a reliable buffer.

Buying online often gives you:

-

Lower premiums compared to offline channels.

-

Easy comparison of term plans, riders, and features.

-

Digital reminders via apps and email.

-

Flexibility to choose high covers like 1 crore term plan or more.

This makes online term insurance ideal for young families needing pure protection without mixing in investment or child savings elements initially.

Revival Options After Lapse

If the policy lapses post-grace period, you can revive it within the revival period (usually 2-5 years, varying by insurer). Requirements typically include:

-

Paying all overdue premiums with interest.

-

Possible health declaration or medical tests.

-

Insurer approval.

Revival restores your original terms. Some insurers offer easier revival windows or reduced formalities for online policies.

Key Tip: Set up auto-debit (ECS/NACH) or calendar reminders to avoid lapses entirely.

Key Takeaways

-

The grace period (15 days for monthly, 30 days for other modes) keeps your policy active and claims payable.

-

Always pay within the grace period to avoid revival formalities.

-

Online term insurance delivers convenience, lower premiums, and high covers like 1 crore term plans.

-

Industry growth, high claim settlement ratios (98%+), and digital trends make 2026 an ideal time to secure protection.

-

Review your policy annually as life stages change (new loans, children’s education, retirement planning).

-

Complement term coverage with separate investment plans, guaranteed return plans, or child insurance plans for holistic financial planning.

-

Set up auto-debit and digital reminders to never miss premiums.

FAQs on Term Insurance Grace Period

It is the extra time (15-30 days) after the premium due date to pay without losing coverage.

Yes, IRDAI sets standard grace periods of 15 days for monthly and 30 days for quarterly/half-yearly/annual modes across life insurance plans.

Yes, valid claims are paid, though the insurer may deduct the unpaid premium from the sum assured.

The policy lapses, and cover stops until revived. You have up to 5 years to revive it.

Yes, by paying overdue premiums with interest and submitting a health declaration. Some cases need medical tests.

The grace period is usually the same (15/30 days), but revival windows may vary slightly.

Annual, half-yearly, or quarterly gives 30 days, while monthly gives 15 days. Choose based on your cash flow.

Yes, including term plans, child insurance plans, and other life insurance plans.

Monthly offers flexibility but shorter grace; annual may save on effective cost.

Yes, with same IRDAI protections, often better features and lower costs.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Other Life Insurance Products

Latest Post

Secure your daughter’s education and marriage in 2026 with LIC’s top child plans. This updated guide has detailed tables, real examples, more features like loans and riders, plus smart tips. Read and plan confidently!

ITR filing for 2026 can feel confusing with income mismatches and form issues. This detailed, simple guide helps working professionals and families avoid costly errors, claim full refunds, and build long-term financial security.

Tax season can be stressful, but avoiding these common ITR mistakes helps you claim rightful refunds faster and stay compliant. Learn practical advice tailored for working professionals and families in India.

Empowering women with financial security! Explore top LIC policies in 2026 tailored for savings, life cover, and family protection. Ideal for working professionals, homemakers, and mothers aged 25-55.

In today’s busy world, keeping track of your life insurance is important for financial security. This easy guide shows how to check your ICICI Prudential policy status quickly so you can manage investment plans, term plans, or guaranteed return plans without stress.

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.