How to Choose the Best Bike Insurance Plan in India?

The thrill of your first ride, the machine shining, and so much more, sounds exciting, right? That's what your new bike will deliver to you. While you enjoy the happiness of buying a new bike, one thing you must not forget is bike insurance.

Since you're already investing a significant sum in your bike, you also need to ensure that you get it protected. That's when you need to purchase bike insurance. Purchasing the best bike insurance India can be confusing, especially with too many options. All you need to focus on is coverage and benefits to get a plan that protects you against unexpected expenses.

How to Find the Best Bike Insurance in India?

While your bike may have third-party insurance, you also need to safeguard your vehicle. That's where you need to purchase the best bike insurance to protect your bike. Conducting thorough research should be of great help in making the right choice.

Here's how you can purchase the best bike insurance India:

1.Coverage Requirement

Before beginning your research for the best insurance plan, you need to learn how much coverage you want. Now, you must base your budget on the coverage you set. A comprehensive coverage would be a safe decision to make today. This way, you receive protection against third-party liabilities and secure your bike.

You should determine the coverage requirement based on how you use the bike. Are there any extra expenditures? Does your bike have any additional liability? You'll have to consider all these factors before making the right choice. Finding a plan that fits your coverage is exceptionally crucial. So, don't just rush into it; take a breather, research, and then choose.

2.Premiums and IDV

Ready to find the best bike insurance plan in India? You must check the premium and the insured's declared value (IDV). Premium is the amount you'll pay for the policy. As for IDV, it is the maximum amount the insurer will pay in case of bike loss or theft.

Premium is something that should fit in your budget. On the other hand, the insurance company may calculate the IDV based on your bike's value. With your bike's increasing age, depreciation will also increase. Therefore, the IDV will also be reduced. This will lead to a lower year-on-year premium. Thus, IDV has a significant impact on your policy premium.

3.Geographical Area

As mentioned earlier, your bike's usage has a significant impact on choosing the insurance plan. Now, you must learn that it's not only about use, but also where it is being used. If you're using your bike in cities, especially for a daily commute, you should consider comprehensive protection.

Comparatively, urban areas have a greater risk of theft and accidents. However, if you'll be using your bike occasionally or in rural areas, you should still not avoid the insurance. In rural areas, there's a risk of accidents due to wildlife, especially if you live near a forest area. Thus, always consider your geographical location before buying the insurance.

4.Review Policy Terms and Conditions

You must always read the policy terms and conditions to understand what is covered and what is not. The policy terms and conditions can help you understand the process of making a claim.

When selecting a bike insurance plan, it's essential to review the inclusions, exclusions, and the claim procedure. Staying informed from the very beginning plays an essential role in offering protection and avoiding any surprises that may arise.

5.Check The Settlement Process

While going through the terms and conditions, you may also want to check the claim settlement process of different insurers. It is advisable to choose insurers that offer a simple process for filing the claim.

The timeline for claim settlement is also an essential factor to consider. The shorter the claim settlement timeline, the better it will be in case of emergencies. Therefore, when the need arises, you can move ahead with the settlement.

6.No-Claim Bonus Schedule

No-claim bonus is one of the most essential components of your bike insurance policy. Under the no-claim bonus, if you don't make any claims, the premiums for the upcoming year upon policy renewal will be reduced.

When choosing a bike insurance policy, it is advisable to choose one that offers comprehensive NCB benefits. Therefore, you'll receive the premium reduction benefits significantly in the upcoming year, as long as you don't file the claim.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Other Motor Insurance Products

Latest Post

You're sitting with your CA on July 28, ready to file your IT return. Your CA asks, "Do you have all investment receipts?" You scramble through documents, realizing some proof is missing. This panic is avoidable.

Buying bike insurance online used to seem complicated. But today, purchasing coverage for your two-wheeler is simpler than ever. The challenge now isn't availability—it's choosing the right bike insurance from dozens of options.

Insurance is an important financial safety net that protects individuals and families against unexpected medical expenses, accidents, loss of income, and other financial risks.

.png)

It's June. The monsoons are here. Suddenly, you develop high fever, body aches, and headache. Your doctor suspects dengue. Your first concern after "Will I be okay?" is "How much will this cost?" This is a question millions of Indians face annually, especially during monsoon and post-monsoon seasons when dengue cases spike.

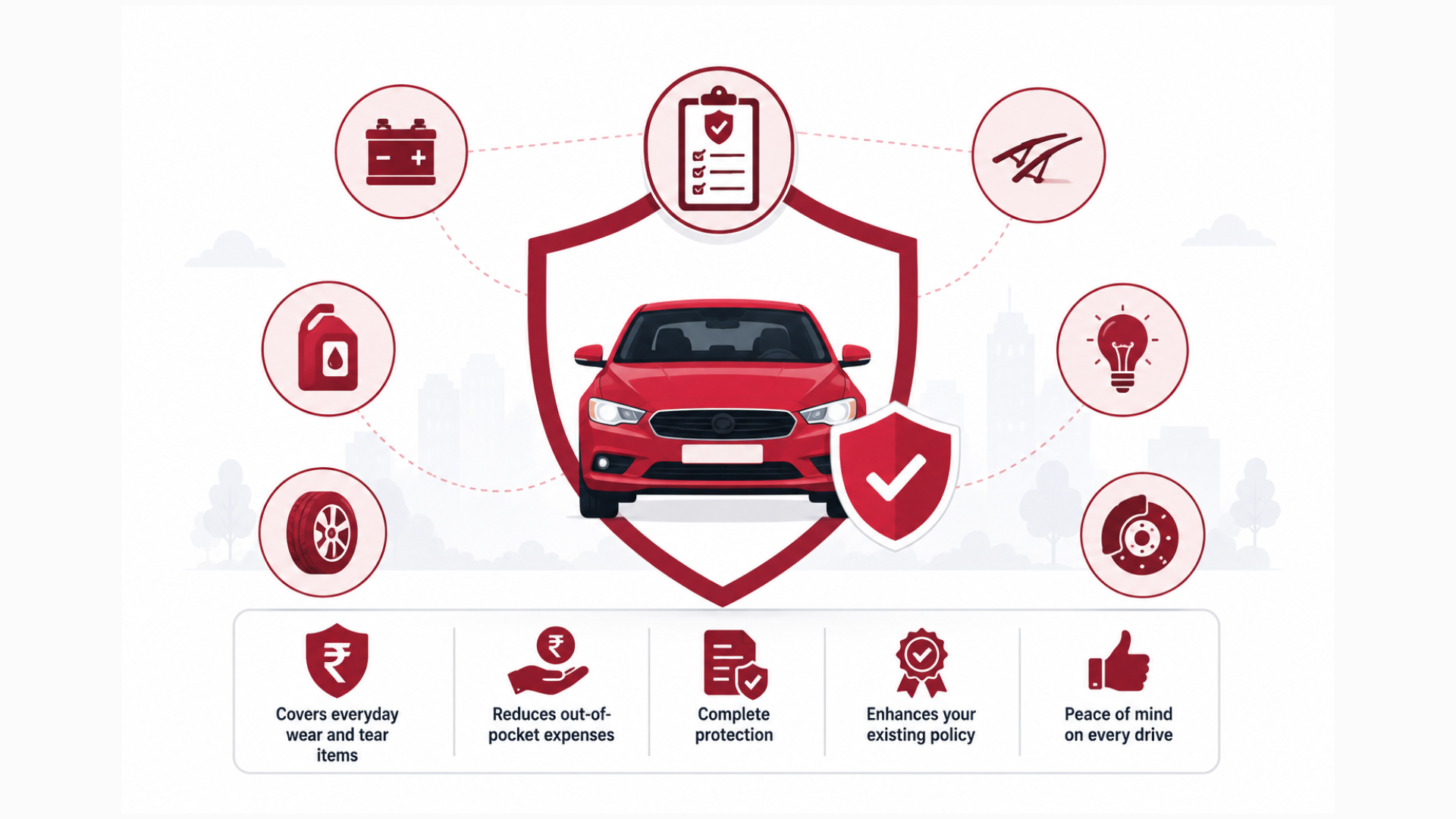

You've just purchased your dream car. You maintain it religiously—regular washing, polishing, timely servicing.

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.