Reasons a Two-Wheeler Insurance Claim gets Rejected

.png)

Do you want to know about the common reasons why a bike insurance claim can get rejected. Read on to know all about claim rejection.

A Bike insurance is a cover that can be procured so that the insurer can meet the legal and financial requirements in the event of a bike accident. But just buying a policy would not be sufficient for getting the compensation if you do not proceed through the claim process successfully. So for a bike insurance claim to be successful there are few factors that an insured must take note of.

Hence, every insurance policy owner should understand some important aspects related to two-wheeler insurance cover which protects them by paying the expenses in the event of an accident. These conditions are such that policy owners should know about them to get knowledge about the restrictions pertaining to their insurance policy which might get their claim rejected.

So, here in this blog, we are discussing the reasons for which a two-wheeler insurance claim can get rejected. Moreover, you will come to know about the mistakes that you are not supposed to make while claiming for a bike insurance compensation in case of an accident.

5 Reasons for a Two-Wheeler Insurance Claim to be Rejected

Below are some of the very common grounds on which a bike insurance claim can be rejected by auto companies, which an insured is supposed to keep in mind while filing a claim:

1. If the Insurance Coverage is not Active Anymore

If your auto insurance policy has expired, in that case the insurer will reject any claim you request, even during the grace period. The insurance companies offer coverage only during the policy period. Thus, it is important for you to renew your auto insurance plan before it expires to continue enjoying two-wheeler insurance coverage on your bike and to be able to file claims. So, if you do not want a two wheeler insurance claim rejection, keep your vehicle insurance policy active all the time.

2. If your claim statement is fake or false

You cannot use insurance to make money. It is not a money making option, rather it is a protection to save yourself from unforeseen expenses. Hence, you cannot take advantage of the various services or benefits of insurance by making false claims. Moreover, the insurance firms carry on ample detailed investigations on receiving a claim before they approve it to assure the authenticity of the request. If a fraudulent claim is filed by a policyholder, he/she can face strict legal action and their claim request also gets canceled.

3. No-Claim Bonus

It is very important to read the offer document of an insurance, be it any insurance plan individual or family. Most people usually do not read the document word-to-word and thus they stay unaware of the inclusions and exclusions of a policy. An insured person with a third-party coverage cannot file any claim for the damages caused to their own vehicle. Further, if an insured has a comprehensive bike insurance, still they may have to bear some expenses from their pocket if he/she doesn’t have any add-on coverage. Thus, in such cases the insurance claims would be considered wrong and the insurance claim is rejected if the insured submit claim with false information.

4. Illegal Actions

For a claim to be approved by the insurance company it is also important that the bike insurance policy holder was not involved in any kind of illegal activities while riding the bike or while the mishap happened. In case of any involvement of the insured in illegal conduct, the claim request gets rejected. Thus, the insured person must ensure that he/she was not under the influence of alcohol or drugs at the time of the mishap. Also, the insured should not be involved in any dangerous stunts or he/she should not be riding the two-wheeler without a proper license and so on. In such cases, the bike insurer would refuse the bike claim and can even terminate the policy.

5. Using Insurance Plan for the purpose of profit

In bike insurance coverage, you can buy plans under two separate categories:

- For individual/ personal two-wheelers

- For corporate vehicles

Hence, you cannot use a personal bike for the purpose of your business as this is termed illegal. So, the two-wheeler insurance company might reject a claim if you use your private vehicle for a commercial purpose and it gets damaged in any accident. Thus, make sure not to use a private car for commercial purposes if you do not want a claim rejection.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Other Motor Insurance Products

Latest Post

You're sitting with your CA on July 28, ready to file your IT return. Your CA asks, "Do you have all investment receipts?" You scramble through documents, realizing some proof is missing. This panic is avoidable.

Buying bike insurance online used to seem complicated. But today, purchasing coverage for your two-wheeler is simpler than ever. The challenge now isn't availability—it's choosing the right bike insurance from dozens of options.

Insurance is an important financial safety net that protects individuals and families against unexpected medical expenses, accidents, loss of income, and other financial risks.

.png)

It's June. The monsoons are here. Suddenly, you develop high fever, body aches, and headache. Your doctor suspects dengue. Your first concern after "Will I be okay?" is "How much will this cost?" This is a question millions of Indians face annually, especially during monsoon and post-monsoon seasons when dengue cases spike.

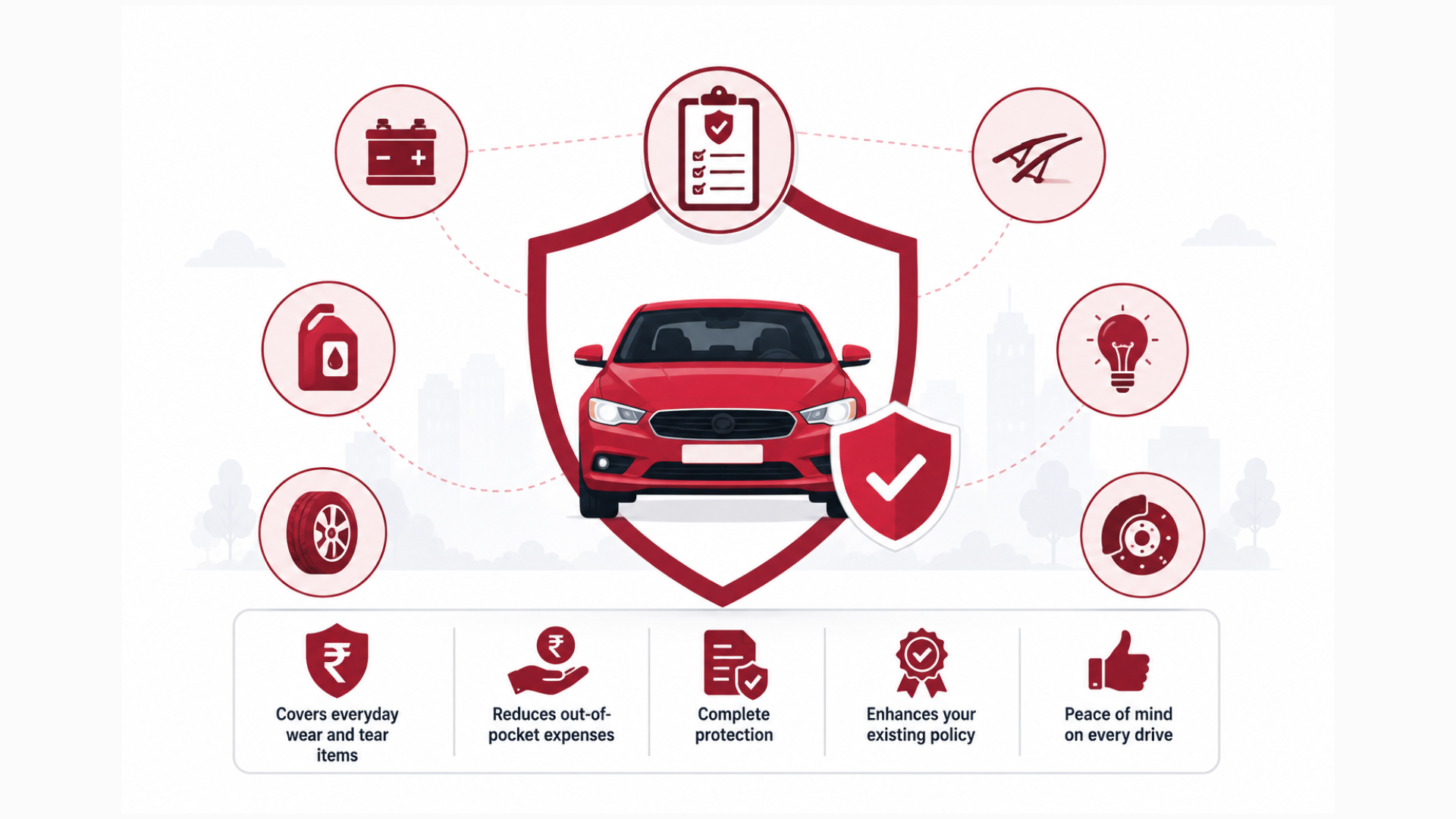

You've just purchased your dream car. You maintain it religiously—regular washing, polishing, timely servicing.

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.