What are the Late Payment Charges and Fee for LIC Premium?

LIC is one of India’s most trusted life insurance providers, offering policies that cater to individuals across all income groups. Whether you own a traditional life insurance plan or a term insurance policy, paying premiums on time is essential to keep your coverage active. In this article, we explain LIC late payment charges, grace period rules, and the policy revival process in detail.

Table of Content

-

Impact of Late Premium Payment on LIC Policy

-

Why Is It Important to Pay LIC Premiums on Time?

-

What Is the Grace Period for LIC Policies?

-

How to Calculate the Late Payment Fees for LIC Premiums?

-

Illustration of Late Fee Calculation Using the LIC Premium Payment Late Fee Calculator

-

What are the LIC late payment charges for premiums?

-

Terms and Conditions of LIC premium payment

-

How to Revive a Lapsed Policy?

-

How to pay your LIC premium to revive it?

LIC has been a trusted brand offering numerous insurance products and services, which cover people adequately irrespective of their economic background. Having an insurance plan from LIC is definitely recommended for all. However, it is also important to know the various requisites of the policies including the late LIC payment charges. Let us understand its importance in detail.

Impact of Late Premium Payment on LIC Policy

Why Is It Important to Pay LIC Premiums on Time?

Paying LIC premiums on time is essential to ensure uninterrupted financial protection and disciplined investment planning. A life insurance policy is not just a protection tool but also a long-term financial commitment that supports future goals such as savings, wealth creation, and family security. Timely premium payments ensure that your life insurance or term insurance policy continues to provide financial protection without attracting additional interest or revival charges.

If premiums are not paid within the due date or the allowed grace period, the LIC policy may lapse. Once lapsed, the policyholder loses critical benefits such as death cover, bonus accrual, and eligibility for loans against the policy. From an investment planning perspective, a lapsed policy can disrupt long-term financial goals and reduce the overall returns expected from the plan.

Delayed premium payments may also attract LIC late payment penalties or require policy revival, which often involves additional costs, documentation, and sometimes fresh medical examinations. This not only increases expenses but also affects the continuity of your financial planning.

To maintain effective investment planning and long-term financial stability, it is important to understand LIC policy terms, track premium due dates, and ensure timely payments. Regular premium payments help keep the policy in force, protect your family financially, and support a well-structured financial future.

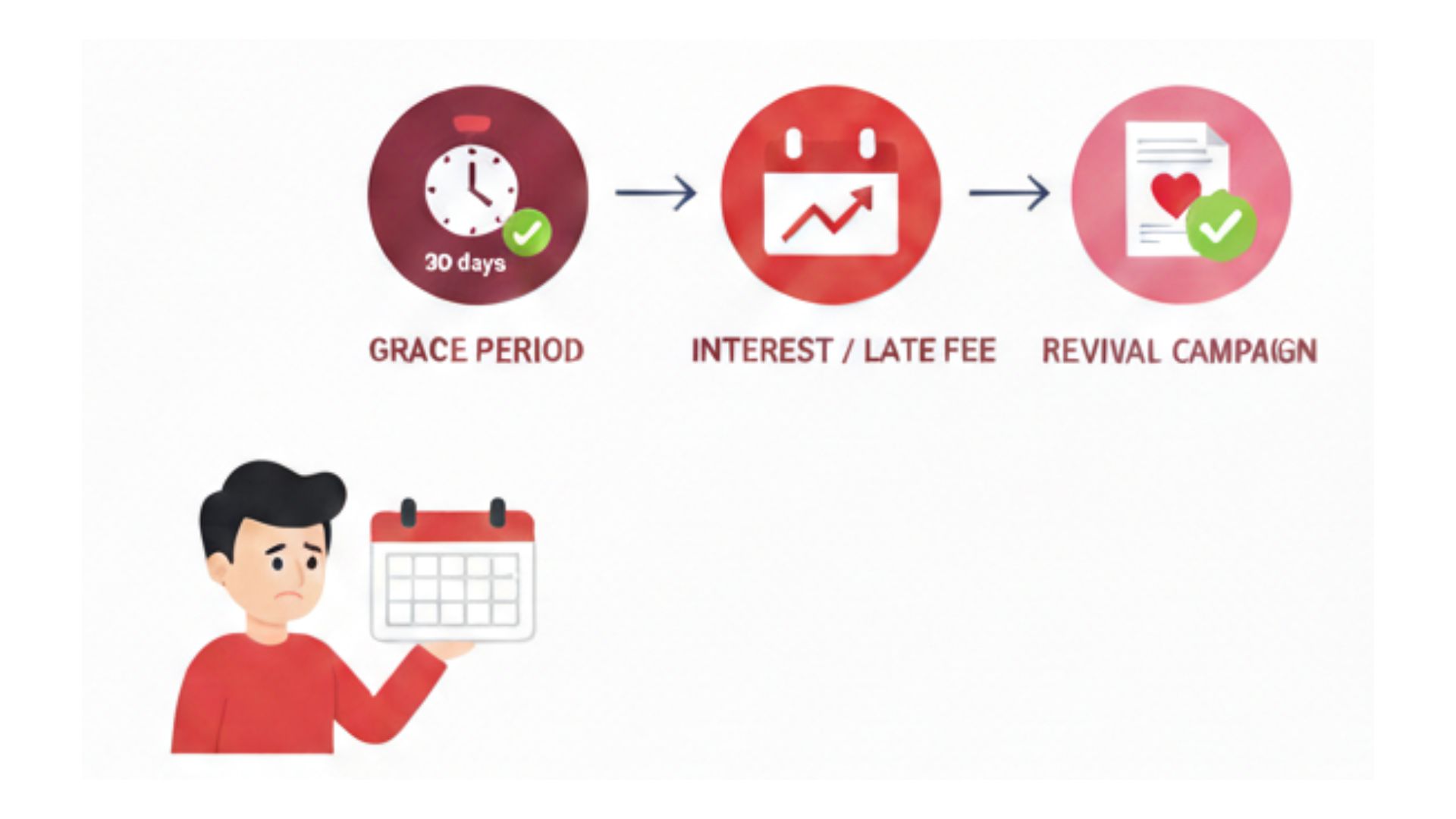

What Is the Grace Period for LIC Policies?

The grace period is the extra time given by LIC to policyholders if they are unable to make the premium payment on time. This is a 30-day time that starts from the end date of the premium payment during which the insured can pay off the overdue amount.

If a policyholder is paying a monthly premium, the grace period allowed is 15 days, whereas for annual premiums, a 30-day grace period is allowed. Policyholders paying premiums during the grace period are not charged any extra fine or fee.This grace period facility is available for all LIC life insurance and term insurance policies. But if the policyholder fails to pay off the amount during this time, LIC will impose a late fee to get the expired policy revived.

How to Calculate the Late Payment Fees for LIC Premiums?

To calculate the late fee for LIC premiums, you can use the LIC Premium Payment Calculator for Late Fees. The calculator considers some factors to evaluate the total late fee amount charged by LIC for delayed premium payments. Below are the details that you must submit:

-

Revival date of the policy

-

Date of the first unpaid premium

-

Amount of premium

-

Premium payment mode

-

Total due (premium) to be paid

-

Interest rate (current)

Based on the above details, the LIC calculator calculates the late payment fees.

Illustration of Late Fee Calculation Using the LIC Premium Payment Late Fee Calculator

To understand how late fees and revival costs are calculated for a lapsed LIC policy in 2026, let’s look at a simple, real-life example.

Assume you own an LIC policy with a monthly premium payment mode. Due to financial or personal reasons, you missed paying your premiums starting January 2025, causing the policy to lapse. In January 2026, you decide to revive the policy and restore its benefits.

The following details are considered for calculating the revival amount:

-

Premium payment mode: Monthly

-

Monthly premium amount: ₹10,000

-

Policy lapsed period: 1 year

-

Applicable interest rate on delayed premiums (2026): 9.5% per annum

Since the policy remained unpaid for one full year, a total of 13 instalments (12 missed months plus the current due month) are pending.

Example: LIC Revival Cost Calculation (2026)

What are the LIC late payment charges for premiums?

Late LIC payment charges levied on a policy premium is calculated as per the time lapse between the expiry date and the subsequent months delayed in making the payments.

Below table will enhance your understanding further on LIC late payment charges:

Terms and Conditions of LIC premium payment

Below are some conditions that are required to be noted regarding LIC premium payment:

- LIC sends reminder notices before the premium due date.

- The premium due date is mentioned in the policy document.

- The responsibility of timely payment lies with the policyholder.

- Grace period: 15 days (monthly mode), 30 days (quarterly/half-yearly/annual).

- After the grace period, the policy lapses and revival with interest is required.

How to Revive a Lapsed Policy?

In case your LIC premium payment due date expires or you fail to make the timely payment even during the grace period and the policy lapses, you still have options of reviving the policy. There are various schemes as explained below that can be followed to revive a lapsed policy.

-

Revival Scheme

-

Special Revival Scheme

-

Loan Cum Survival Scheme

-

Survival Benefit Cum Revival Scheme

Let’s understand them in detail one by one.

# Ordinary Revival Scheme – Under this scheme, the policyholder is required to pay the arrears of all the unpaid premiums of his/her LIC policy in one single payment with interest. There are various terms and conditions that need to be considered while reviving your LIC policy via this scheme. You are also required to offer a good health declaration form along with a medical certificate if required

# Special Revival Scheme – This scheme allows the Date of Commencement (DOC) of the policy to move in a way that the policy doesn’t lapse. So, you can make the payment within the revival period in one single premium. Other documents like medical certificates might also be required like in the above case. Further, you must note that:

-

the revival should be done within 3 years of policy lapse

-

this scheme is allowed only once during the term of a policy

-

the policy shouldn’t have surrender value

# Survival Benefit Cum Revival Scheme – This scheme is used mainly to revive the money back policies. Here, the policyholder can use the survival benefit gained from the policy to revive it. However, this is possible if the date of receiving survival benefit is before the revival date. If the survival benefit amount is less as compared to premium due, the policyholder is expected to make the additional payment from his/her pocket. And if the survival benefit amount is more than the due payment, the extra amount is paid back to the policyholder.

# Loan Cum Survival Scheme – Under this scheme, if the customers of LIC policy have acquired a surrender value on the policy, he/she can take a loan against it to revive the lapsed policy. Thus, you can pay the premium arrears as a loan from the accumulated amount available.

How to pay your LIC premium to revive it?

There are two ways to make your LIC policy premium payment. They are online and offline.

1. Online payment methods include:

-

Official LIC portal – Payment can be done by visiting the official LIC portal and using online banking facilities like debit or credit card, UPI, wallets etc.

-

Authorized Banks – There are many authorized banks that accept LIC premium payments. Some of these banks are namely; Axis Bank, Union bank, IDBI bank etc.

-

Merchant Mode – Merchant modes can also be used to make premium payments. Some of them include authorized agents known as Empowered Point, Retired LIC Employee collection points, LIC associates etc.

-

Franchisees – Franchisees are also available to make payments such as Paytm, AP Online, InstaPay etc.

2. Offline payment methods include:

-

NACH – NACH or National Automated Clearing House is a payment option that can be utilized by LIC policyholders to make payments. Under this payment mode, your bank deducts LIC premium at a pre-decided date, which is then remitted to LIC

-

Bill Pay – Bill Pay or EBPP (Electronic Bill Presentment and Payment) is a process under which an LIC statement is sent to the policyholder electronically. The customer then pays the premium via several electronic mode of ayments at his/her dispersal

-

ATM – ATMs of Axis Bank and Corporation banks can also be used by LIC customers to make payments of premiums

Key Takeaways

- LIC provides a 15–30 day grace period for premium payment.

- No penalty is charged during the grace period.

- After grace period, interest is applied on delayed premiums.

- Policy revival requires payment of pending premiums plus interest.

- Timely premium payment keeps your life insurance and term insurance benefits active.

LIC Premium Late Fee and Charges

To pay LIC premium after due date, you can:

1. Visit the official website of LIC

2. Go to Online Premium Payment option on the home page

3. Click on the tab of Pay Direct

4. You can select the LIC Renewal of premium or revival of policy option as per need

5. Now choose the Proceed button and make the payment

It is done

If your LIC of India payment due date expires and you miss out on paying the premium, you can use the grace period to make the payment. Here's the process to make the payment online:

# Visit the official website of LIC

# Click on Online Premium Payment option on the home page

# Go to Pay Direct tab

# Now opt for the Premium Renewal or revival of policy option as per need

# Choose the Proceed button and make the payment

If you miss the grace period to pay your LIC premium payment, your policy will lapse. In that case, to revive a lapsed policy, you might have to pay a penalty in the form of extra fees as well as might have to go through the renewal process of the policy once again.

Yes, you can pay your insurance premium during the grace period if you miss the last date of payment. However, It might lapse if you miss the payment during the grace period.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Other Life Insurance Products

Latest Post

Empowering women with financial security! Explore top LIC policies in 2026 tailored for savings, life cover, and family protection. Ideal for working professionals, homemakers, and mothers aged 25-55.

In today’s busy world, keeping track of your life insurance is important for financial security. This easy guide shows how to check your ICICI Prudential policy status quickly so you can manage investment plans, term plans, or guaranteed return plans without stress.

Not too long ago, many Indian families viewed insurance as an optional investment or something only needed in old age. However, a major shift is happening across the country. Today, having a comprehensive health policy is no longer just a choice—it has become a financial necessity for every single household.

Recent scientific breakthroughs have reignited a fascinating and controversial question: Can parents one day choose specific traits for their babies, such as intelligence, height, athletic ability, or disease resistance?

Discover why Mumbai is bucking the national trend with rising HIV deaths in 2026, even as Maharashtra and India report a significant decline. This easy-to-understand guide covers the latest NACO statistics, key reasons behind Mumbai’s challenge, and practical prevention steps for working professionals aged 25 to 55.

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.