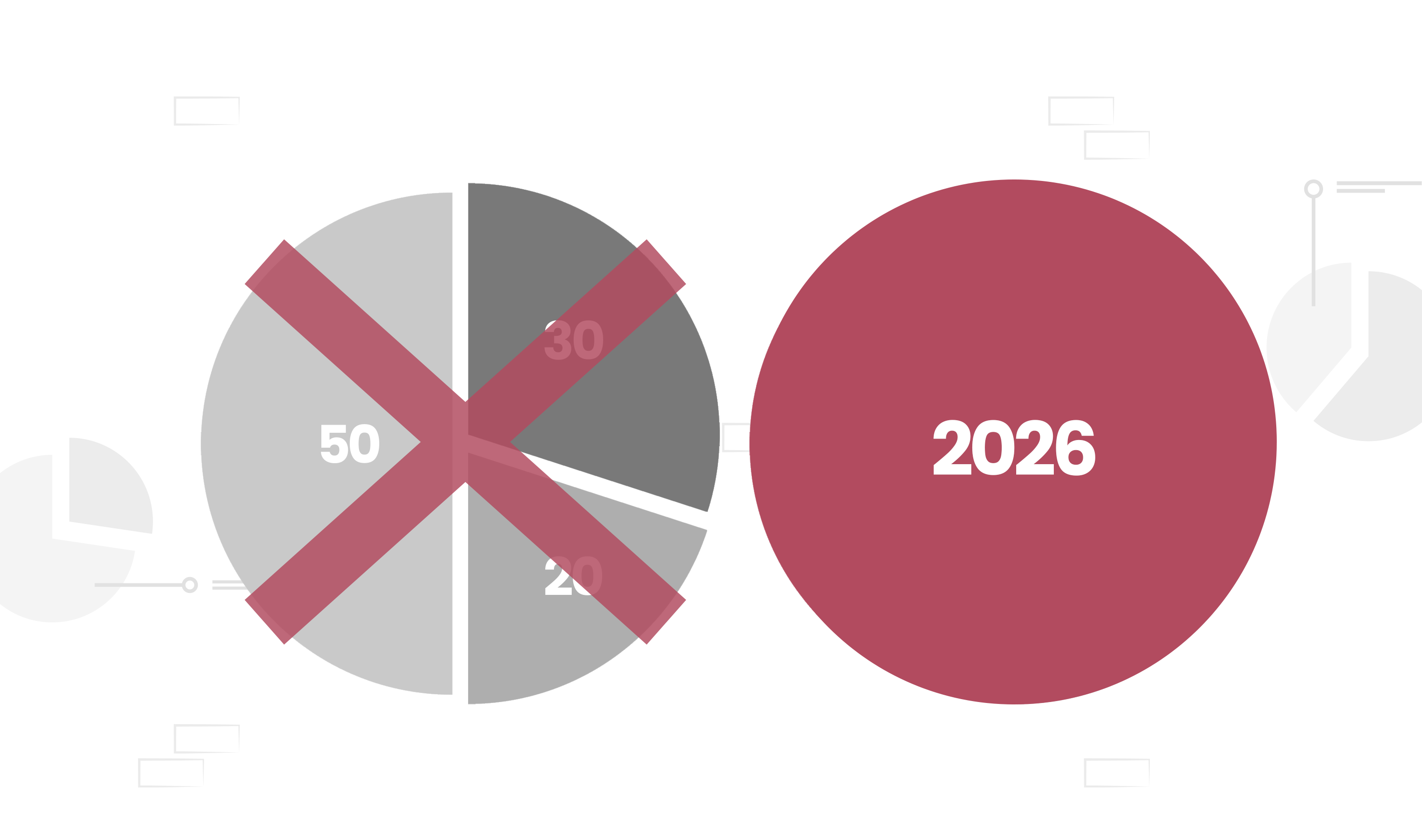

Budgeting 2026: The Old 50/30/20 Rule Is Dead

Once upon a time, budgeting felt simple. Earn your salary. Split it neatly. Feel responsible. The 50/30/20 rule became so popular because it sounded doable, even comforting. But welcome to 2026. Rent has opinions. Groceries have grown egos. EMIs show up like uninvited relatives. Suddenly, that tidy formula feels out of touch with reality.

You are not bad at managing money. The rules just haven’t kept up. Income patterns have changed. Expenses have multiplied. Lifestyle inflation quietly moved in without paying rent. Budgeting today needs flexibility, not fixed ratios carved in stone. It needs to work for real lives, not textbook examples. So yes, the old rule had a good run. But it’s time to think again about how we are managing our finances.

Why Budgeting Feels Harder in 2026

Before we talk about rules, let’s understand what changed.

What Is the 50/30/20 Rule?

The 50/30/20 rule divides your total income into three buckets. Fifty per cent of it goes to needs. Think rent, groceries, electricity, school fees, and EMIs. Thirty per cent is for wants. This includes dining out, OTV subscriptions, shopping, travel and all the other things that make your life enjoyable. The remaining twenty per cent is allotted to investments and savings.

On paper, it looks elegant. No complicated math. No endless tracking. Just a road discipline. For multiple years, this budgeting approach has worked reasonably well, especially when your income rose faster than your expenses. It helped new professionals and first-time earners understand finances without feeling overwhelmed.

Example of 50/30/20 in 2026

But the rule assumes something important. That your needs will politely stay within half your income. In 2026, that assumption is optimistic. Housing costs alone can eat far more. Add healthcare, insurance, and education, and the balance tilts quickly. The rule isn’t wrong. It’s just outdated. Like budgeting with a calculator when the problem now needs a spreadsheet.

Limitations of the 50/30/20 Rule

The biggest issue is rigidity. Life rarely fits clean percentages. A higher rent city laughs at the idea of fifty per cent needs. The rule also ignores income stages. A fresh graduate, a mid-career professional, and a self-employed individual do not spend the same way. Yet the rule treats them equally.

It also oversimplifies savings. Twenty per cent may be too little for someone starting late or too much for someone rebuilding finances. Worst of all, it gives guilt. When numbers don’t fit, you feel like you failed. In reality, the rule failed you.

New Budgeting Rules

The 70/20/10 Rule

This rule flips the script. Instead of forcing low needs, it accepts reality. Seventy per cent of your income goes toward living expenses and lifestyle combined. Rent, food, bills, small joys, all included.

Twenty per cent is dedicated to savings. No excuses. This covers your emergency funds, investments, and other long-term goals. The remaining ten per cent is set for personal priorities and flexible spending. Think of hobbies, travel or even aggressive debt repayment.

Why does this plan work? Because it reduces stress. You stop constantly reshuffling money between needs and wants.

Everything lives together, realistically. It suits people in expensive cities or those balancing multiple responsibilities.

Sample Allocation (₹80,000 Income)

This rule isn’t about restriction. It’s about sustainability. You save money consistently without feeling deprived of your rights. And consistency, not perfection, is what builds wealth.

The 80/20 Rule

The 80/20 rule is refreshingly simple. Focus on saving twenty per cent of your income first. The remaining eighty per cent is yours to manage as you see fit.

This approach works well if you dislike micro-budgeting. Once savings are automated, guilt disappears. You know progress is happening. Everything else becomes flexible.

It also adapts easily to variable income. Freelancers, consultants, and business owners often prefer this method. When income rises, savings rise. When income dips, the system adjusts naturally.

The key here is discipline at the start. Savings must happen before spending. Not after. This rule trusts you to manage the rest responsibly. And surprisingly, many people tend to do better with mild flexibility than with rigid limits.

The Zero-Based Budget Rule

Zero-based budgeting gives every single rupee a job. Here, income minus expenses should equal zero. That doesn’t mean you spend everything. It means savings are treated as an expense.

This method is detailed. You assign money to rent, food, travel, investments, insurance, and even fun. Nothing floats unaccounted for. It’s perfect if you love control or want to fix leaks. Overspending becomes visible. Bad habits stand exposed.

When to Use Zero-Based Budgeting

The downside? It requires effort. Regular tracking is essential. But the payoff is clarity. You know exactly where money goes and why.

For people serious about financial goals, this method can be transformative. It turns budgeting into awareness, not restriction. And awareness changes behaviour faster than guilt ever will.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 21 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Latest Post

Buying a car doesn't always mean breaking the bank. If you're looking for an affordable vehicle that doesn't compromise on quality or reliability, 2026 is a great year to make your purchase.

Statins are among the most commonly prescribed medications worldwide for reducing cholesterol and preventing serious cardiovascular diseases such as heart attacks and strokes.

Explore everything about the All-India National Permit in 2026. This detailed guide helps truck owners, fleet operators, and transporters understand fees, types, application steps, government rules, and tips to stay compliant while saving time and money on interstate logistics.

Commercial vehicles are the backbone of India's transportation and logistics industry. From trucks carrying goods across states to taxis, buses, school vans, ambulances, auto-rickshaws, and delivery vehicles serving daily commuters and businesses, these vehicles play a vital role in the country's economy.

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.